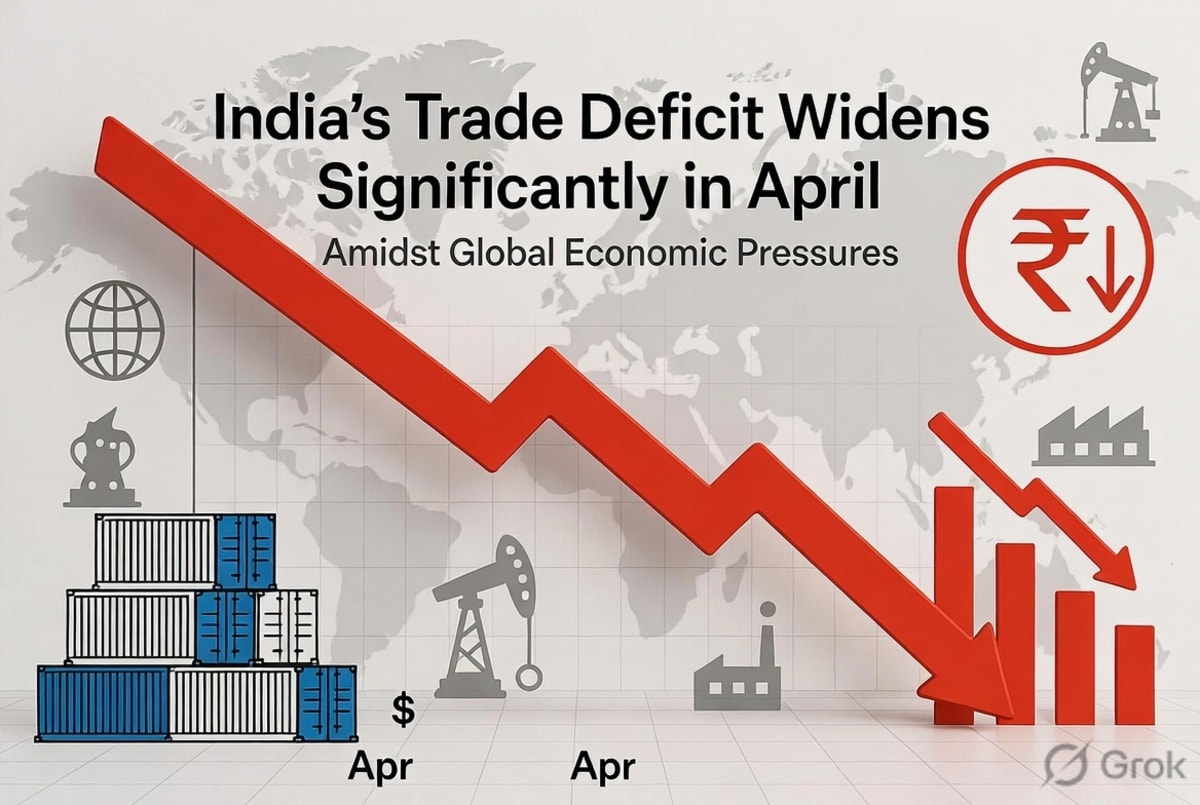

India's trade deficit widened considerably in April 2026, reaching $28.38 billion, a significant jump from the $20.67 billion recorded in March. This expansion in the trade gap, announced by the Ministry of Commerce and Industry, underscores the persistent economic headwinds India is navigating, influenced by global supply chain disruptions and elevated energy prices. The surge in imports, which climbed to $71.94 billion from $59.59 billion in March, outpaced the growth in merchandise exports, which rose to $43.56 billion from $38.92 billion.

Impact of Geopolitical Tensions on Import Costs

The escalating conflict in the Middle East has had a pronounced effect on India's import bill. As a major importer of crude oil and cooking gas, India is particularly vulnerable to disruptions in the West Asian region, which accounts for a substantial portion of its energy supplies. Oil imports alone surged to $18.62 billion in April, a sharp increase from $12.18 billion in March, directly contributing to the wider trade deficit. Similarly, gold imports saw a significant rise, reaching $5.63 billion compared to $3.06 billion in the previous month, reflecting underlying demand and potentially hedging against currency volatility.

Services Sector Provides Partial Cushion

While the merchandise trade balance experienced a widening deficit, India's robust services sector offered a partial counterbalance. Services exports were estimated at $37.24 billion in April, a notable increase from $32.85 billion in the same month last year. Services imports, however, stood at $16.66 billion. The net contribution from services trade helped to mitigate the overall impact on the current account, though not enough to offset the substantial rise in merchandise imports.

Currency Pressure and Policy Considerations

The widening trade deficit has placed additional pressure on the Indian rupee, which has experienced depreciation against the US dollar. This currency weakness, coupled with persistent external sector concerns, has made the rupee one of the weakest-performing Asian currencies in 2026. The government and the Reserve Bank of India (RBI) are closely monitoring these developments. While the RBI has maintained a neutral monetary policy stance, keeping the repo rate unchanged at 5.25% in its April 2026 meeting, the central bank remains vigilant to inflationary pressures and external shocks. The RBI has projected CPI inflation for the current financial year at 4.6%, with upside risks from elevated energy prices and potential El Niño conditions.

The Ministry of Statistics and Programme Implementation reported that India's overall inflation rate (CPI) inched up to 3.48% in April 2026, a slight increase from 3.40% in March. This figure, while below market expectations, indicates a steady upward trend, particularly in food inflation which rose to 4.20%. The government's efforts to manage the economy include focusing on export promotion and supply chain resilience, aiming to cushion the blow from global trade tensions and geopolitical instability. Looking ahead, the World Bank projects India's GDP growth to accelerate to 7.6% in FY26, despite global headwinds, but forecasts a moderation to 6.6% in FY27, partly due to the ongoing Middle East conflict. The nation's economic trajectory will continue to be shaped by its ability to manage import costs, bolster exports, and navigate the complex global economic landscape.